Readings Newsletter

Become a Readings Member to make your shopping experience even easier.

Sign in or sign up for free!

You’re not far away from qualifying for FREE standard shipping within Australia

You’ve qualified for FREE standard shipping within Australia

The cart is loading…

This title is printed to order. This book may have been self-published. If so, we cannot guarantee the quality of the content. In the main most books will have gone through the editing process however some may not. We therefore suggest that you be aware of this before ordering this book. If in doubt check either the author or publisher’s details as we are unable to accept any returns unless they are faulty. Please contact us if you have any questions.

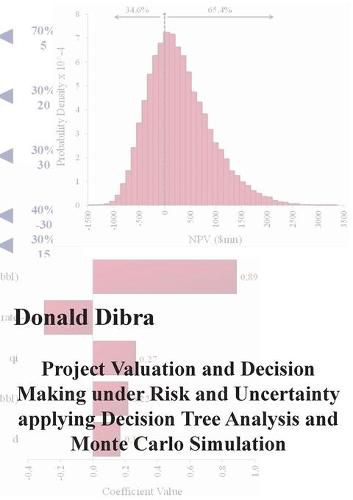

This work presents the application of the Monte Carlo Simulation method and the Decision Tree Analysis approach when dealing with the economic valuation of projects which are subjected to risks and uncertainties. The Net Present Value of a project is usually used as an investment decision parameter. Using deterministic models to calculate a project’s Net Present Value neglects the risky and uncertain nature of real life projects and consequently leads to useless valuation results. Realistic valuation models need to use probability density distributions for the input parameters and certain probabilities for the occurrence of specific events during the life time of a project in combination with the Monte Carlo Simulation method and the Decision Tree Analysis approach. After a short introduction a brief explanation of the traditional project valuation methods is given. The main focus of this work lies in using the Net Present Value method as a basic valuation tool in conjunction with the Monte Carlo Simulation technique and the Decision Tree Analysis approach to form a comprehensive method for project valuation under risk and uncertainty. The extensive project valuation methodology introduced is applied on two fictional projects, one from the pharmaceutical sector and one from the oil and gas exploration and production industry. Both industries deal with high risks, high uncertainties and high costs, but also high rewards. The example from the pharmaceutical industry illustrates very well how the application of the Monte Carlo Simulation and Decision Tree Analysis method, results in a well-diversified portfolio of new drugs with the highest reward at minimum possible risk. Applying the presented probabilistic project valuation approach on the oil exploration and production project shows how to reduce the risk of losing big.

$9.00 standard shipping within Australia

FREE standard shipping within Australia for orders over $100.00

Express & International shipping calculated at checkout

This title is printed to order. This book may have been self-published. If so, we cannot guarantee the quality of the content. In the main most books will have gone through the editing process however some may not. We therefore suggest that you be aware of this before ordering this book. If in doubt check either the author or publisher’s details as we are unable to accept any returns unless they are faulty. Please contact us if you have any questions.

This work presents the application of the Monte Carlo Simulation method and the Decision Tree Analysis approach when dealing with the economic valuation of projects which are subjected to risks and uncertainties. The Net Present Value of a project is usually used as an investment decision parameter. Using deterministic models to calculate a project’s Net Present Value neglects the risky and uncertain nature of real life projects and consequently leads to useless valuation results. Realistic valuation models need to use probability density distributions for the input parameters and certain probabilities for the occurrence of specific events during the life time of a project in combination with the Monte Carlo Simulation method and the Decision Tree Analysis approach. After a short introduction a brief explanation of the traditional project valuation methods is given. The main focus of this work lies in using the Net Present Value method as a basic valuation tool in conjunction with the Monte Carlo Simulation technique and the Decision Tree Analysis approach to form a comprehensive method for project valuation under risk and uncertainty. The extensive project valuation methodology introduced is applied on two fictional projects, one from the pharmaceutical sector and one from the oil and gas exploration and production industry. Both industries deal with high risks, high uncertainties and high costs, but also high rewards. The example from the pharmaceutical industry illustrates very well how the application of the Monte Carlo Simulation and Decision Tree Analysis method, results in a well-diversified portfolio of new drugs with the highest reward at minimum possible risk. Applying the presented probabilistic project valuation approach on the oil exploration and production project shows how to reduce the risk of losing big.

Search our extensive online catalogue.